Most foreign travellers lose money in India before they spend a single rupee on something they actually want. It happens at the airport counter, at the ATM, and at every merchant where an international card gets declined with no explanation. The forex card you loaded before flying felt like a smart move. India has quietly made it the most expensive one.

UPI has replaced cash and cards for over 55 million merchants across India, and foreign travellers now have a direct way in. Before you board your flight, knowing which payment method cuts your costs, which one actually works at street level, and which combination gives you zero declined payments could save you thousands of rupees on a single trip.

Key highlights

- India has over 55 million UPI-enabled merchants. Most small vendors, street food stalls, and local markets accept QR payments only.

- Forex cards typically carry ATM withdrawal fees, cross-currency markups of 3% to 5%, and no merchant QR payment capability.

- CheqUPI is free to join for all eligible nationalities. The wallet loading fee is 2.95% + applicable taxes for all foreign users. There are no transaction fees when paying merchants through UPI.

- CheqUPI’s per-transaction cap is Rs 1,00,000, and the monthly spending cap is Rs 3,00,000.

- UPI wallets for foreign travellers support Person-to-Merchant (P2M) payments only, not person-to-person transfers.

- Your forex card still earns its place. Use it for ATM cash, hotel check-in holds, and airport spending. Use UPI for everything else.

What is a forex card, and how does it work in India?

A forex card is a prepaid travel card loaded with currency before your trip. You swipe it at card terminals or use it at ATMs, and the card draws down your pre-loaded balance. In India, it works at most hotel chains, major airports, large retail stores, and international restaurant chains.

Where forex cards work in India

Forex cards run on Visa or Mastercard rails and are accepted at any point-of-sale terminal that supports those networks. That covers most four and five-star hotels, large supermarkets like Reliance Fresh and D-Mart, international brands like Starbucks, and domestic airline counters. ATMs across India, including SBI, HDFC, ICICI, and Axis, accept foreign-issued Visa and Mastercard.

Where forex cards fall short

The problem is that India’s payment infrastructure has skipped the card terminal entirely for millions of merchants. A local autorickshaw driver, a street food vendor, a government museum ticket counter, a temple prasad shop: all of these are likely UPI-only. Card acceptance in informal and semi-formal sectors is close to zero. If you rely on your forex card alone, you will need cash for a significant portion of your daily spending, and ATM withdrawals come with fees that add up fast.

ATM charges for foreign cards in India typically include a fixed fee from your home bank, a cross-currency conversion markup ranging from 3% to 5%, and a local ATM operator surcharge. On a Rs 10,000 withdrawal, the combined cost (including bank fees and markups) typically ranges from Rs 500 to Rs 900, depending on your home bank or more, depending on your card issuer.

What is a UPI wallet for foreign travellers, and how does it work?

A UPI wallet for foreign travellers is a Prepaid Payment Instrument (PPI) licensed by the Reserve Bank of India. It gives you a UPI ID tied to a wallet balance, so you can scan any merchant QR code in India and pay instantly, just like a local. You do not need an Indian bank account.

How CheqUPI bridges the gap

CheqUPI is an RBI-licensed UPI wallet built specifically for foreign travellers and NRIs. You download the app, complete a quick, one-time in-person verification step after you arrive in India, and load funds using your international credit or debit card. From that point, you scan and pay at any of India’s 55 million+ UPI merchants, from a roadside biryani stall to a hotel spa. The wallet is built on Transcorp International’s PPI (Prepaid Payment Instrument ) and Authorised Dealer Category II licence, backed by Y Combinator (W22).

What the loading fee actually costs you

CheqUPI charges a loading fee of 2.95% + applicable taxes for all foreign users. If you load below Rs 10,000, an additional Rs 150 applies. On a Rs 20,000 load, the total fee is approximately Rs 700 to Rs 750, including tax. Merchant payments via UPI after that point are free.

Compare that to an ATM withdrawal using a typical forex card: a Rs 20,000 withdrawal with a 4% cross-currency markup plus a Rs 200 ATM fee costs roughly Rs 1,000. The UPI wallet loading fee is lower and covers your entire trip’s merchant spend, not just a single cash withdrawal.

Forex card vs UPI wallet: fee comparison

| Feature | Forex card | CheqUPI UPI wallet |

| Loading / funding cost | 3% to 5% markup on conversion + ATM fees | 2.95% + applicable taxes for all foreign users. |

| Merchant payment fee | Zero (swipe at card terminals) | Zero (UPI QR scan) |

| ATM withdrawal | Rs 200 to Rs 500 fixed fee + 3% to 5% markup | Not applicable |

| Merchant acceptance in India | Large hotels, airports, major chains | 55 million+ merchants, including street vendors and local shops |

| P2P transfers | Not applicable | Not supported for foreign national wallets |

| Monthly spend cap | Depends on the card issuer | Rs 3,00,000 |

| Per-transaction cap | Depends on the card issuer | Rs 1,00,000 |

For the most current CheqUPI fees, visit chequpi.com/faqs.

Planning your India travel budget? Our travel guide has a full cost breakdown by trip type.

Where each payment method works

In practice, neither option alone covers every situation in India. The country operates across two parallel payment systems, and knowing which one applies where saves you money and stress.

Forex card wins here

Use your forex card at international hotel chains and five-star properties, especially for check-in holds. Use it at large airport retail and duty-free. Use it for booking domestic flights or train tickets online. Use it at any merchant with a physical card terminal running Visa or Mastercard. If you need emergency cash quickly and there is no time to top up your wallet, an ATM withdrawal on your forex card is the fastest fallback.

UPI wallet wins here

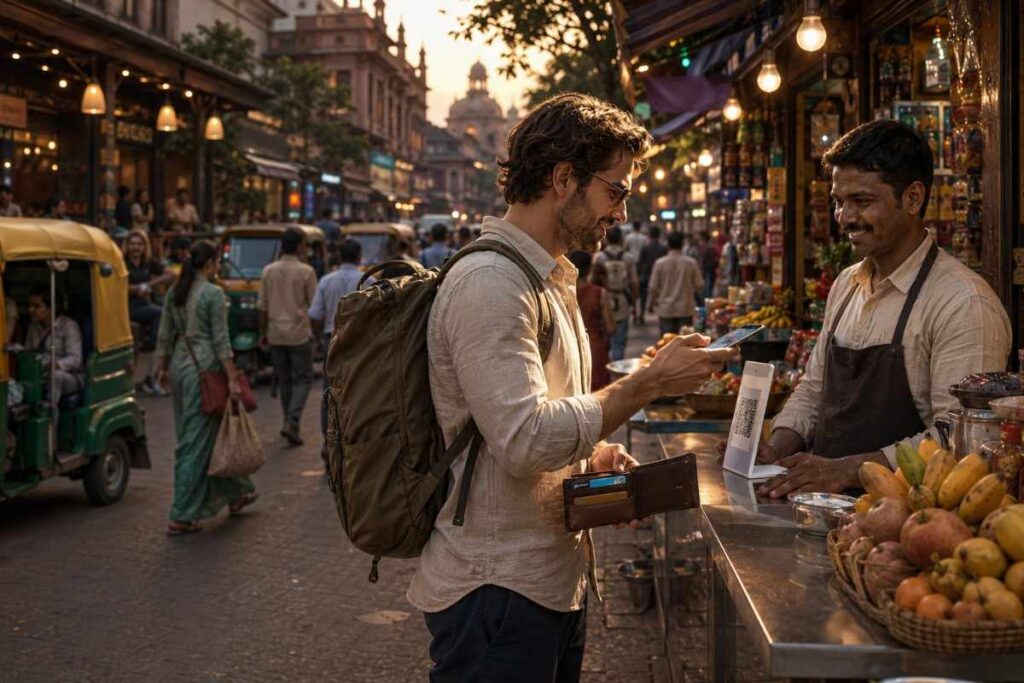

A UPI wallet covers the bulk of daily tourist spending in India. Street food, local restaurants, heritage site entry tickets, auto-rickshaws and tuk-tuks, souvenir shops, pharmacies, petrol pumps, and most neighbourhood grocery stores are UPI-only or UPI-preferred. In destinations like Varanasi, Jaipur, Kochi, Goa, and Agra, etc a significant share of the tourist-facing economy runs entirely on QR codes.

For more on staying safe with your money in India, see our safety guide for foreign travellers.

Transaction limits to know before you travel

CheqUPI wallets for foreign travellers operate within RBI-mandated limits for Prepaid Payment Instruments. These are fixed by the regulator, not by the app.

- Per-transaction cap: Rs 1,00,000 (approx $1,060)

- Daily spend cap: Rs 1,00,000 (approx $1,060)

- Monthly spend cap: Rs 3,00,000 (approx $3,170)

- Daily transaction count: 10 transactions

- New user restriction: Rs 50,000 (approx $530) cap and 5 transactions for the first 24 hours

Note: Cooling-off period (the 1st 24 hours) starts from the 1st transaction (not from activation).

For most tourist trips, these limits are more than adequate. A two-week holiday in India would need Rs 3,00,000 in monthly wallet spend only if you are staying in high-end accommodation and spending heavily every day.

One important rule: CheqUPI foreign tourist wallets are restricted to Person-to-Merchant (P2M) payments. You cannot transfer funds to another person’s UPI ID or bank account. For all merchant QR payments, the wallet works exactly as expected.

Which payment method is right for you

Neither one replaces the other. The smarter question is how to combine them for your specific trip.

Use a UPI wallet if you plan to

- Eat at local restaurants, dhaba-style places, or street food markets

- Travel by auto-rickshaw, cycle rickshaw, or local app-based cabs

- Shop at local bazaars, craft markets, or government emporiums

- Visit temples, museums, or heritage sites that use QR ticketing

- Stay at guesthouses, homestays, or mid-range hotels

Keep a forex card for

- International hotel check-in holds and incidental charges

- Large purchases where a card receipt is needed for expenses

- Online bookings for domestic flights or trains before you arrive

- Emergency ATM withdrawals if your wallet balance runs low

The practical setup most foreign travellers find works well: load Rs 15,000 to Rs 25,000 onto a UPI wallet after activation(KYC), use it for day-to-day spending, and keep the forex card for hotels and online bookings.

Conclusion

India’s payment ecosystem is built around UPI. A forex card gets you through airport arrivals and hotel check-ins; a UPI wallet gets you through the actual trip. The loading fee on CheqUPI is lower than most ATM withdrawal costs on a forex card, and the merchant coverage is dramatically wider. Carry both, use each where it fits, and you will not get stuck at a QR code with empty hands.

FAQs

What is the best payment method for foreign travellers in India in 2026?

A combination works best. Use a UPI wallet like CheqUPI for daily merchant payments and a forex card for hotel check-ins, large purchases, and ATM cash when needed.

Can foreign travellers use UPI in India without an Indian bank account?

Yes. RBI-licensed UPI wallets like CheqUPI let foreign travellers load funds using international cards and pay any UPI merchant without needing an Indian bank account.

What are the fees on CheqUPI compared to a forex card?

CheqUPI charges a loading fee of 2.95% + applicable taxes for all foreign users. Merchant payments are free. Most forex cards charge a 3% to 5% currency conversion markup plus ATM fees on each withdrawal.

Is CheqUPI free to join?

Yes. CheqUPI is free to join for all eligible nationalities.You can check the eligible nationalities list here.

What is the monthly spending limit on a CheqUPI wallet?

The monthly cap is Rs 3,00,000 (approx $3,170). The per-transaction limit is Rs 1,00,000 (approx $1,060), and the daily cap is Rs 1,00,000.

Can I use a forex card at street food stalls and local markets in India?

Generally no. Most street vendors, local markets, and informal merchants in India accept UPI QR payments only. A forex card requires a card swipe terminal, which most small vendors do not have.

What is the difference between Niyo and a UPI wallet for Indian foreign travellers?

Niyo is designed for Indian residents travelling abroad. CheqUPI is designed for foreign travellers arriving in India. They solve opposite problems on opposite ends of the same journey.

Does CheqUPI support person-to-person transfers?

No. Foreign national wallets under RBI guidelines support Person-to-Merchant (P2M) payments only. You cannot transfer funds to another individual’s UPI ID.P2P transactions are not supported

How do I load money onto a CheqUPI wallet?

You load funds via your international credit or debit card through the app. CheqUPI charges a loading fee of 2.95% + applicable taxes for all foreign users. Merchant payments via UPI cost zero.

Is a UPI wallet safer than carrying cash in India?

For most situations, yes. A UPI wallet gives you a digital transaction record, lets you track spending in the app, and removes the risk of carrying large amounts of cash. That said, keep Rs 5,000 to 10,000 in cash for remote villages and very small informal vendors where QR codes may not be available.

“You can access India’s UPI network immediately after a quick verification step. CheqUPI takes minutes to set up, works at 55 million+ merchants, and costs less per rupee spent than most ATM withdrawal routes.

Download CheqUPI. Activate your wallet after arriving in India and start paying with UPI in minutes.”